As an estate planning attorney, a question that I am asked -- which I used to be asked much more frequently - is what are some pain free ways (translation: not having to hire an attorney) to shield my estate from estate taxes?

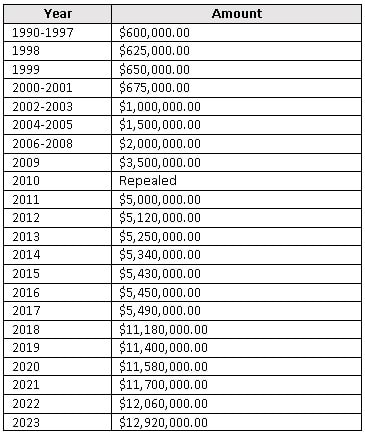

Before I directly answer that question, some recent history is helpful. Through 1997, the unified credit was $192,800 which equaled an exemption amount of $600,000 per person. In other words, estate taxes were calculated on the amount of the decedent's assets over $600,000. The following chart shows the growth of the individual credit during the last 30 plus years. As can easily be seen there has been a significant growth in the amount that an individual can have before his/her estate is subject to estate tax. A married couple has double the amount or $25,840,000 estate tax free. With that being written, the law is slated to "sunset" on December 31, 2025 and then the exemption reverts to $5.49 million (the 2017 amount) adjusted for inflation. So, what are some easy things that can be done? Give the money away while alive (must be careful with appreciated assets); leave to charity; utilize the annual gift tax exclusion which in 2023 is $17,000 to give gifts to as many people as one wants; and make payments directly to educational (pay the tuition of grandchildren) and medical providers on behalf of loved one. Even for extremely wealthy people these are effective ways to reduce the estate tax burden. SOME THINGS WILL NEVER CHANGE.

LIKE THE RISING AND SETTING OF THE SUN, AMERICA'S FAVORITE PASTIME, OR TAXES, PEOPLE OFTEN FAIL TO SEE THE VALUE IN ESTATE PLANNING. ARETHA FRANKLIN WAS UNFORTUNATELY ONE OF THESE INDIVIDUALS. SHE PASSED TWO MONTHS AGO OF PANCREATIC CANCER AND Left not only a great legacy, but also an $80 Million Dollar Estate, and FOUR SONS. SHE CERTAINLY KNEW SHE WAS SICK, BUT CHOSE NOT TO PUT HER THOUGHTS DOWN ON PAPER. HER four SONS AGE’s range from 48 TO 63. UNDER THE LAWS OF MOST STATES—including michigan—WHEN A DECEASED PERSON HAS NOT WRITTEN A WILL, AND THERE IS NOT A SPOUSE, THE CHILDREN INHERIT EQUALLY. IN HER CASE the lack of an estate plan is made even more PREVALENT because of the condition of her eldest son. He IS INCAPACITATED, AND RECEIVES BENEFITS FROM THE STATE OF MICHIGAN; HAD MS. FRANKLIN Left her ESTATE in will and trust, HE WOULD HAVE BEEN ABLE TO CONTINUE RECEIVING THOSE BENEFITS. as if it were not already enough, her estate is now Subject to probate. THE DISTRIBUTION OF HER ESTATE WILL also PLAY OUT PUBLICLy and be AVAILABLE for anyone to ACCESS. Additionally, the amount the government would receive from her estimated $80 million dollar estate could have been minimized. THE IRS IS ENTITLED TO 40% OF THE ESTATE AFTER THE FIRST $11,180,000. ON AN $80 MILLION ESTATE, THAT IS OVER $27 MILLION DOLLARS. I COULD GO ON . . . BUT THE MESSAGE IS CLEAR, MS. FRANKLIN WOULD HAVE GOTTEN MORE RESPECT HAD SHE HAD AN ESTATE PLAN PREPARED BY AN ESTATE PLANNING ATTORNEY! As an estate planning attorney, frequently I have clients’ whose parents have not prepared their own estate plan. There are a couple of reasons as to why people procrastinate in this area. The first reason is that some people feel that by preparing an estate plan they are jinxing themselves and may “die” – the thought is some variation of the following: “if I do nothing I will live. Once I prepare something, I will die”. For virtually everyone, it requires confronting their own mortality. Some are ready to confront their mortality while others are not so ready.

The reality is for most people with assets if they do nothing it is likely that their estate will have to go through probate. While our office is very efficient at handling probates, it is not something most heirs enjoy. What if you do not know if your parents have done estate planning? Obviously, the easiest way to find out is to ask them. However, for some children that is a difficult question. They may feel that they are appearing to be greedy. It is possible that some parents do not want to be asked and feel like their privacy is being invaded. One approach is to turn the question around and indicate to them that they are thinking about doing their own estate planning and inquire as to who they used for their own estate planning. Maybe discussing the situation with a sibling is the way to proceed. That is especially true if the parents have a better relationship with the sibling or if they believe that sibling is more financially stable. Some parents are very open to involving their children in their own affairs. I have seen parents ask a child to begin handling their financial affairs including being responsible for bill paying even when the parents are still able. Some parents never ask and children discover bills not being paid for months at a time. For obvious reasons, it is important that once parents start showing evidence of mental decline and serious forgetfulness that there be a system in place to make sure that finances are being properly handled. While it does not happen frequently, I have counseled children as to how to the approach to take with their parents after listening to their family’s situation. Life is interesting. It frequently comes full circle. The people who brought us in to the world need our help at the end. There has been a lot written since Prince passed about the fact that he had not done estate

Planning. Much of what has been written is to the effect that had he done an estate plan it would be a lot easier to distribute his estate. That may or may not be correct. When one dies and does not leave a will or a trust, he is said to have died “intestate” and the laws of intestacy of his state of residence control the distribution of his estate. Each state has its own law of intestacy. In most states if you are a single person, without children, your estate would go to your parent(s). Since neither of Prince’s parents are alive, the default is to his siblings. For most people that is straightforward, but Prince has a number of half siblings and at least one of them has predeceased him. Most states provide that if a sibling predeceases you, that siblings share goes to his child or children. Still not all that difficult. What is complicating the situation at the moment, is that while Prince did not have any known living children, there are people who contend that Prince is their biological father. DNA testing is going to be utilized to assist the Carver County District Judge in making his determination as to whether Prince did or did not leave a child or children. Under the law of most states that child or those children would jump to the very front of the line and inherit his estate. Even with a trust and a will, individuals could certainly have contended that they were fathered by Prince and the same process would have occurred. The failure of Prince to have engaged in estate planning will undoubtedly result in less money going to his heirs because Uncle Sam and the state of Minnesota will receive more money than they would have if he had engaged in comprehensive estate tax planning. In California individuals with a net worth greater than $5,450,000 have estates that are subject to estate tax. Unlike Minnesota, California does not impose a state “death tax”. Minnesota’s state estate tax is 16% and is imposed on estates with a value greater than $1,600,000. So ultimately, Prince’s estate which has been publicly estimated to be valued between $300,000,000 and $500,000,000 will pay over 50% of its worth in taxes. Most people would say that it would have been worth a couple of visits to the estate planning attorney to save $150 to $250 million. His heirs, whomever, they turn out to be will receive a lot of money, but they could have almost double had Prince engaged in comprehensive estate planning. I was reading an article recently about a very wealthy family in Australia that had to deal with the passing of the patriarch of the family. Everything went incredibly well. The attorney for one of the two children, Steven Glanz, has represented some of the wealthiest individuals in Australia and he has found that three things help make the process smooth regardless of the size of the estate. I agree wholeheartedly with his first two principles and would modify his third. Failure to do these three things increases the risk that siblings will be upset with each other long after the patriarch is gone.

Every now and then I will write a post about a celebrity who has passed away, and whether or not their Estate Plan was effective (if there was a plan in place at all). While the Estates of the rich and famous are significantly larger than most of my clients, the lessons that are learned from their mistakes are important to note.

This is not a complete list by any means; my hope is that by reviewing some mistakes that have been made in the past, they can be prevented for you and your estate.  Like almost anything in life, reverse mortgages can be great if utilized correctly and can result in financial chaos if used incorrectly.

Reverse mortgages are marketed to older Americans as a means for people to have some extra money so that they may live comfortably. Borrowers must be at least 62 years of age and must live in the home. With a reverse mortgage, the homeowner always retains title to their property. However, they may have little to show for it. The negative to reverse mortgages is that while the borrower most of the time is not required to repay the loan provided they are living and stay in the home, upon death or moving from the home, the lender frequently becomes the virtual owner of the home.

We all know that eventually someone is going to have to deal with the issues concerning our funeral and/or memorial service; burial or cremation. As with other parts of estate planning, we have the ability to make things much easier on our loved ones by doing a little planning ahead of time.

When our office prepares an estate plan for a client, we provide them with a section in their estate planning binder to make their wishes known to their family. This includes notifying specific family members, friends, and organizations of the individual's passing. We also provide forms for our clients to set forth their personal information; sections for handling of remains and marker selection; casket or urn selection; information concerning a remembrance/funeral service; and information regarding costs and expenses. In the United States for the last twenty-five years certain wealthy families have been taxed differently than other wealthy families solely as a result of when the wealth was accumulated.

Trusts have been around for hundreds and hundreds of years. Even living trusts have been around for a long time. Today estate planning attorneys in most states routinely recommend a living trust to their clients. For example in California – it does not matter if a client is in Los Angeles, Manhattan Beach, Culver City or anywhere else in the state – it has been this way for well over twenty years. In the eastern United States, it has been a shorter period of time.  Estate Planning attorneys are sometimes asked to prepare premarital agreements. When I am asked, it is usually because at least one of the spouses is “older” or is because it is a second marriage for at least one of the spouses.

People often attempt to take shortcuts in the execution of premarital agreements. Shortcuts can invalidate the agreement. In California, premarital agreements have to meet certain requirements for them to be considered valid by the court in the event the marriage dissolves and one party seeks to implement the agreement. Obviously it is an important issue! Many business owners have created a very successful business by working incredibly hard to develop something that is worth a fair amount of money. Unfortunately, a lot of these same people have not implemented a succession plan.

Many of these same people do have an Estate Plan, including a well drafted Living Trust – obviously some do not – but it is silent regarding the business. When planning ahead to protect the legacy that you have created, creating a thoughtful business succession plan is vital. Depending on the size and nature of the business, it may require the company's CPA, a financial advisor, an insurance professional, and an estate planning attorney. Watch out for those estate planning attorneys! Linda Nell Lowney was an estate planning attorney for many years. In 2005 she became romantically involved with a client of hers, Thor Tollefsen.

Mr. Tollefsen was in his mid-eighties and 30 years older than Ms. Lowney, had emphysema and terminal cancer, and was using a walker when he married her in 2006. They married under a confidential marriage license that wrongly stated that the two were living together. Shortly after they were married, Mr. Tollefsen complained to relatives that his wife was not taking care of him as she had promised to do and he began living in a senior care facility. When he died, his relatives discovered that Lowney had the remainder of the $340,000 that he had transferred to her less than 2 years earlier expecting that she would pay for his care with the money. Ms. Lowney had argued before the State Bar of California that she had been given the money as his girlfriend and not as his attorney. |

Categories

All

Michael Burstein

Estate Planning and Probate Attorney, Manhattan Beach Local, Sports Enthusiast

Archives

April 2023

|

RSS Feed

RSS Feed

|

|

LOS ANGELES

3611 Motor Avenue, Suite 220 Los Angeles, California 90034 Tel: (310) 391-1311 Fax: (310) 391-4853 |

MANHATTAN BEACH

111 North Sepulveda Blvd. Suite 250 Manhattan Beach, California 90266 Tel: (310) 545-7878 |

Connect With Us

|